The Grande Butterfly

Happy Sunday 👋

If you’re reading this but haven’t subscribed, join our growing community here 👇

Last Monday, stock markets around the world had their worst day in half a year just to recover the losses in the second half of the week. The consensus is that the stumble was caused by Evergrande, a Chinese real estate developer who is about to default on his debt and may go bankrupt.

But how can some real estate company in China make your shares in Disney (-3.8%), BMW (-4.5%) or Glencore (-6.5%) drop? This is what we cover today.

The Story 👉 What’s Happening At Evergrande

The Economics 👉 Systemic Risk

The Technicals 👉 Options Volatility Contagion

Let’s go!

The Evergrande Story

The Evergrande Group is a Fortune 500 real-estate developer based in Shenzhen, China. In 2020, it had sales of >$100 billion.

As a developer, Evergrande has a highly cash-consumptive business model. Building new real estate can take many months and requires a lot of cash along the way. Cash collections (from buyers) come later, with the exception of smaller upfront deposits.

Evergrande funded its impressive growth mostly through debt - it borrowed aggressively, even by real estate property development standards.

It became the world's most heavily-indebted developer, with obligations of more than $300bn to creditors and other businesses.

The debt-fueled growth opened the doors for Evergrande (and its now billionaire founder) into an elite class. It entered the Fortune 500 at #496 in 2016 and reached #122 by the latest ranking. But debt is a double-edged sword—and Evergrande was due to catch the other edge.

For over twenty years, Evergrande was China’s largest developer, riding the country’s property boom. Banks and investors were happy to bet on China’s growing middle class and its appetite for homes and other properties.

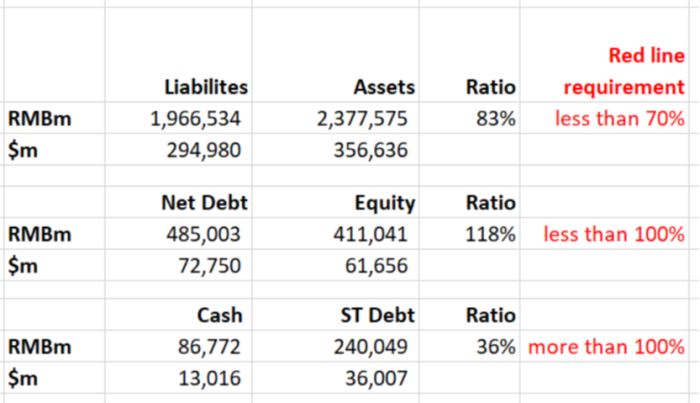

Because of particularly high debt levels in the real estate market, the Chinese government imposed “three red lines” on property developer balance sheets in August 2020. The new rules said: Companies must have a liability/asset ratio <70%, a net debt/equity ratio <100%, and a cash/short-term debt ratio of at least 1.

If companies fail all three thresholds, they are forbidden from taking on additional debt. Here is how Evergrande scored at the end of June:

So Evergrande was prohibited from borrowing more money, which means it could not refinance existing debt with new debt and needed to start repaying loans out of its own pocket.

As a result, Evergrande and other players are now lacking the money to finish building houses, leaving families without the homes for which they had already paid.

In 2020, the company even pushed employees to provide short-term loans to the company or risk losing their year-end bonuses.

Now, hundreds of employees and panicked home buyers are demanding their money back from Evergrande, gathering outside the company’s offices across China last week.

The Economics

With deep ties to financial institutions and working class consumers across China, a disorderly collapse would impact suppliers, banks, employees, retail investors and others parties.

The government is now in a tough spot. It could bail out Evergrande and be viewed as condoning the financial excess that led to the problem, or allow the collapse to ripple through the entire economy that is just recovering from COVID shocks of 2020/21.

The company has $142bn in short-term payables and there are a lot of suppliers across China (cement, copper, tiles companies), who are waiting for payment that may never come.

And what if the Evergrande mess shakes confidence in the property market?

Decreasing real estate prices, combined with the inability to take on new debt could lead to a series of defaults from Chinese developers.

Ming Tan, director at Standard & Poor’s who follows Chinese banks, said the main risk for China’s financial system would be “other highly leveraged developers to default at the same time.”

This could start a domino effect.

The shares of China’s biggest insurance company, Ping An, fell by as much as 8.4% on Monday, after closing down 5% the Friday before. Even though Ping An does not have any direct exposure to Evergrande’s debt or equity, it is linked to the country’s real estate market through its ca. $600bn insurance funds.

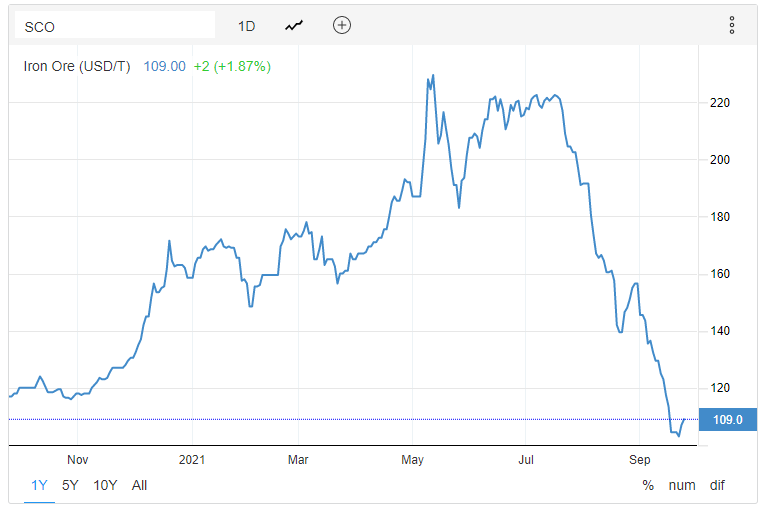

Metal prices are also falling due to concerns around the Chinese property market. With falling real estate prices, there would be less construction and lower demand for metals. Iron ore, which is a vital source of profit for major mining companies around the world, dropped by 25% since the start of the month.

As a result, mining stocks were among the biggest losers on the FTSE 100 in London on Monday.

It was a panic spiral.

Most people however agree that Evergrande will not become a systemic event because they believe that the Chinese government can solve debt problems more or less at will. The Communist party can tell the state-owned commercial banks to roll the debt over, restructure it, forgive it or whatever.

“In our base case scenario, China Evergrande will be allowed to collapse with the most profitable parts of its business bought up by rivals and the debt underwritten by either the [People’s Bank of China] directly, or by a consortium of Chinese commercial banks with the help of a liquidity injection by the PBOC.” - Joachim Klement and Susana Cruz of Liberum

Some variation of this scenario seems most likely. China’s financial system is mostly self-contained. That means debt is often owed by one part of the country to another and the government controls all of those parts.

The Technicals

Why were companies even in seemingly unrelated industries affected?

Conventionally, we see the a current market price as an equilibrium resulting from a tie between buyers and sellers. This construct is generally stable, unless a ton of people decide to switch sides all of a sudden. When more buyers join, the price increases until more sellers join or some buyers leave.

However, this picture does not consider stock options, which have their own dynamic. Specifically we need to look at dealer's hedging activity.

Options 1.1: When you buy a call option on a stock, it gives you the right to buy a stock at an agreed price in the future. If the share price goes up, you can exercise the option, buy the stock at the agreed price and sell it in the market at a now higher price to make a profit.

But what about the other side of the deal?

The broker who sold you the option may not want to hold this risk. So to hedge his position, he simultaneously buys the stock in the market when selling you the call option. So when you exercise your call option he already has the stock which he can then sell you.

If the stock price decreases, he will have a small loss from the stock, but also the gain from the option which he sold you that offsets the loss.

This drives up the stock price because the broker is actively buying shares to hedge his position. The larger your call position, the more shares the broker buys for hedging and the higher the share price rises.

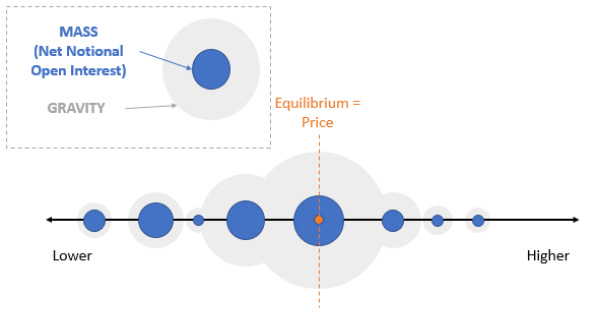

You can conceptualize this dealer’s hedging dynamic as a mass placed along the price axis. The mass has a specific gravity. A big mass close to the current price will have a strong gravity - while a big mass far away from the current price has a weaker gravity.

If you buy a call option with an exercise price far out of the money your bet has a low probability of making money, so the dealer may decide to take the risk and leave his position unhedged - or at least partially.

The further out the exercise price is, the smaller the fraction of the position that the broker will hedge.

It’s a probabilities game.

That’s why the gravity effect changes with volatility (among other factors). Greater volatility means there is a higher likelihood of the price moving far enough for the option to be in-the-money. This increases the risk for the broker, which leads to more hedging. More hedging means more buying activity. That’s the gravity effect.

Okay, so higher volatility means out-of-the-money options have a stronger pull on the stock price. Good to know but who really cares?

Well, this is where things get interesting.

Volatility drives investors away. So volatility and price are strongly negatively correlated. This negative correlation is key.

As volatility increases, prices are expected to decrease. So when there is an external event like a global pandemic or the threat of domino-ing bankruptcies in the Chinese real estate market, volatility and options hedging spike, causing a catalyst for falling stock prices.

Downward pressure spirals until prices are so low that enough new buyers come in an create a new price equilibrium.

At this point, markets calm and volatility decreases. Lower volatility means less risk for brokers, who start to slowly unwind their hedges again, leaving to a recovery.

This is what happened last week.

Financial markets are linked like we never seen before, driven by passive funds. Evergrande shares are held by about 130 equity-based ETFs and a dozen fixed income ETFs. The debt ETFs alone have an aggregate asset volume of $26bn.

Everyone now has indirect exposure to everything and companies like Evergrande can cause butterfly effects like the one we saw last Monday.

Even if your Disney, BMW or Glencore stocks may have nothing to do with Chinese real estate, they may fall short term if overall volatility increases in the stock market. In these cases, things will typically self-correct, so whatever you do, don’t panic sell.

NEWS | OPPORTUNITIES | BITES

Crypto Crackdown

China has declared all activities related to digital coins illegal. Even overseas cryptocurrency exchanges are now prohibited from providing online services to residents in China. Link

Face-Ban

Facebook is partnering with Rayban for a large-scale commercial launch of sunglasses with cameras, speakers and a microphone starting at $299. This is an essential stepping stone for FB’s AR glasses. Video

Ant Group Gets Broken Up

Beijing has ordered Ant Group to split off its multi-billion-user app Alipay, which accounts for ~40% of Ant’s total revenue. Link

Chip Shortage

The global semiconductor scarcity which has impacted automakers for over a year now seems to be getting worse. New coronavirus outbreaks in Southeast Asia led to shut downs of chip assembly lines, causing more car companies and electronics manufacturers to stop production. A flood of new delta-variant cases is causing production delays at chip suppliers in Malaysia, Vietnam, and the Philippines. Link

Interest Rates

The Fed said it could soon slow its large-scale purchases of government-backed bonds and indicated it might raise interest rates already in 2022. Surprise. Link

New Apple Toys

Apple hosted a virtual event and announced a new generation of your most favorite toys: iPhone 13, Apple Watch Series 7, New iPad & iPad Mini. All the details here.

NEWS | OPPORTUNITIES | BITES

Active

Datadog (DDOG), Pexip (PEXIP), ECOMI (OMI)

NEWS | OPPORTUNITIES | BITES

🚀 From $0 to $7.75bn - in 2 years

📰 Walmart does not accept Litecoin as payment

🕵️ SEC gives $110m award to whistle blower

🐋 Land-roaming whales

💳 Why everyone loves “buy now, pay later”

Was this forwarded to you? You can get your own copy sent to your inbox every week.

If you find this newsletter interesting and know people who might enjoy it, it would mean a lot if you forward it on 🙏

Sources: Financial Times, ETFGI, WSJ, Bloomberg, @TheLastBearStanding, Trading Economics

I am long PEXIP, OMI, DDOG. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

I am not a registered investment, legal or tax advisor or a broker / dealer. All investment / financial opinions expressed by me are from personal research and experience and are intended as educational material. Although best efforts are made to ensure that all information is accurate and up to date, occasionally unintended errors and misprints may occur.