Datadog

Datadog

A Crack in Apple's AppStore Armour. Bad News for Chinese Teen Gamers. CEO Change and Insider Buying at Pexip.

Happy Sunday 👋

if you are new, welcome and feel free to join a growing list of subscribers here 👇

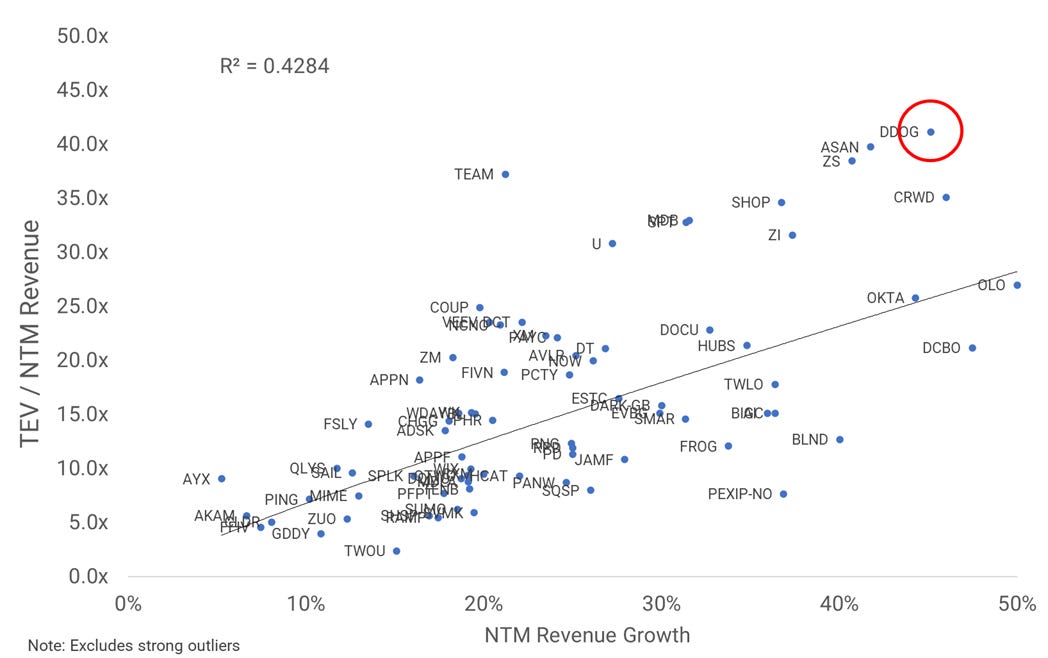

Q2 earnings season is over. One of the best performing companies with a strong surprise on both revenue and EPS was Datadog (DDOG). I took a closer look at the company and explain why I believe there is still a lot of upside potential, despite a high price tag.

Let’s go!

NEWS | OPPORTUNITIES | BITES

Apple has been forced to make some changes to its app store policies in response to an investigation by the Japan Fair Trade Commission. The new policies mark the first step towards Apple losing its near-monopoly position over accounts processed in its App Store. Link

Additionally, South Korea will allow local app developers to avoid Apple’s 30% sales commission. Link

These changes don’t directly impact Apple's largest markets, but they are small cracks in the company’s heavy armour.

The Chinese government now prohibited underage children from online gaming on school days and allows a max of 1h / day in the evening on weekends to prevent young people becoming addicted to video games. Companies like Tencent are using facial recognition to enforce the new rule. Link

Alibaba is playing good citizen and committed to invest $16 billion in fostering social equality and “common prosperity” in an effort to stand in President Xi Jinping’s good graces when the next corporate crackdown comes. Link

NEWS | OPPORTUNITIES | BITES

Datadog is a leader in monitoring solutions for cloud-scale applications. They're seeing rapid growth in a large addressable market that's benefiting from digital transformation. Despite the fact that competition has recently increased, Datadog continues to grow its customer base. Their product development speed is incredible, with the number of paid solutions more than doubling in the last year. They have more opportunities in adjacent markets in the future. Two technical co-founders lead the company. I'll investigate the company's history, finances, product portfolio, target market, and competitive landscape. This will lay the groundwork and provide an investment framework for investors to track Datadog's progress in the future.

Datadog provides a “cloud-based monitoring and analytics platform for developers, IT operations teams, and business users.” - S1

With solutions for monitoring, traces, and logs, they claimed to be the first company to address the "three pillars of observability" in one toolset.

The term "Observability" has gained a lot of traction over the last year, but what does it mean exactly in the cloud space?

For large enterprises, when a site-wide technical issue arises, engineers need to troubleshoot quickly to find the source of the problem. Dedicated Observability teams are formed to create a central system to capture, store, query, and visualize performance data from all of the company’s services, and to quickly analyze all of this data to determine what service behavior was the root cause.

Monitoring is a part of observability. Monitoring gathers relevant performance data from systems and services to reflect their current state of operation. From CPU levels to query response times, performance data can cover a wide range of indicators.

Log analysis is another aspect of monitoring. Every software service keeps track of its activities in some way. System logs (events at the operating system level), security logs (resource access events), and application logs are all examples of this.

Traces are the third aspect of monitoring. Traces show how a request progresses through the code of an application. A customer request for a specific web page on a website is a common trace. The trace would show every step of the request processing, from the web server code to database queries to calls to any external services, such as Facebook or credit card processing. The trace depicts each step in the process as well as the time it takes. This creates a "waterfall" view, which allows a system operator to quickly follow the trace and identify potential bottlenecks.

Observability is a tool that combines monitoring and context in one package. It ensures that all relevant service performance data is captured and visualized, as well as providing the context needed to quickly sort through the data and identify anomalous behavior for troubleshooting. Over the last years full observability of systems has become a necessity.

Datadog arrived in this rapidly changing market at the right time and with the right strategy. They took advantage of the observability trend by providing monitoring as well as context. They offer one solution for all relevant systems – applications, server infrastructure, network, and third-party services in all types of hosting configurations. They were the first to provide a comprehensive solution that encompassed all of these dimensions in a single, consolidated view.

Datadog was able to leapfrog the leading point solution providers, such as New Relic for tracing and Splunk for logging, by combining these use cases into one solution and marketing the "three pillars of observability." These businesses are scrambling to expand their observability scope, while Datadog is quickly gaining market share. Elastic is the only other company that has emerged with a holistic solution along a similar path. In the competition section, we'll go over all of these options.

The trends that are driving the need for observability are unlikely to slow down in the future. Businesses of all sizes will continue to invest in digital transformation as customer expectations for higher service levels rise.

Q2 2021

Datadog released its Q2 2021 performance on August 5th. The report was excellent, reflecting a return to the high-growth revenue trajectory that investors had become accustomed to prior to COVID. Datadog outperformed forecasts on both the top and bottom lines in the second quarter, and boosted its projections for the third quarter and the rest of the year. Following the results, the stock jumped 15% after having been flat for the previous 12 months. DDOG is already up more over 55% in 2021, and I expect it to finish the year substantially higher.

I'll go over the main important takeaways from the quarter in the parts below, with more specifics in the areas after that.

Revenue growth is accelerating. After a 51% increase in Q1, revenue increased 67% in Q2. This outperformed expectations of a 52% increase by 15%. With a 60% increase predicted for Q3, actual Q3 growth could be closer to 70%. Growth was driven by a 36% increase in total customers paired with a dollar-based net retention (DBNRR) of over 130 percent. Datadog is adding new customers at a rapid rate and then increasing their spend over time effectively. Customer spend expansion accounted for 70% of Q2's revenue gain YoY. Full year guidance was also revised to 56% growth. Keep in mind that the initial Q4 forecast was for a 38% increase.

Billings and RPO (remaining performance obligations) exceeded revenue, indicating future revenue growth. A 103% increase in total RPO demonstrates Datadog's ability to sign multi-year contracts.

FCF margin was 18%, and Non-GAAP operating margin was 13%, indicating continued operating leverage at scale.

R&D spending has increased by 85% YoY and now accounts for 30% of total income, compared to S&M’s 26%, the lowest among peers. This indicates that DDOG can continue investing in R&D while keeping S&M costs low.

Product delivery speed is increasing. Database Monitoring came out post-earnings, DDOG launched Application Security in Beta and unveiled another monetization product in Cloud Workload Security. These are in addition to the previously announced CSPM and the basic Security Monitoring solution. On the observability front, they also announced CI Visibility (beta) and Dash is coming in October.

Growth

Revenue for the second quarter was $233.5 million, up 66.8% YoY and 17.6% sequentially, exceeding analyst expectations of $212.4 million, or 51.7% YoY, as well as the company's previous Q1 estimate of $211 million to $213 million.

In the third quarter, additional acceleration is expected. At the midpoint, Datadog forecasts sales growth of 59.7% YoY. Based on the Q2 surprise of +15%, actual Q3 growth might come in even higher.

DDOG raised its full-year guidance to $938 million to $944 million, representing a 55.9% increase over 2020. Guidance was increased from 46.6% in the first quarter and 38% at the start of the year.

For the second quarter in a row, Datadog increased its ARR by nearly $100 million. Management announced that APM and log management had a combined ARR of $400 million and were still in "hypergrowth" mode.

Land & Expand

According to Datadog's 10-Q, existing customers accounted for roughly 70% of revenue growth, with new customers accounting for the remaining 30%. This underlines the significance of their land & expand motion.

Customer spending scales with consumption and many of Datadog's customers are digitally native disruptors who are experiencing significant development themselves. Peloton, Airbnb, Instacart, Fiverr, Coinbase, DraftKings, Wayfair, and Zillow are just a few examples. Customers typically begin with 1-2 of Datadog’s products like infrastructure monitoring or logging and gradually add more such as APM, network monitoring, user experience, and other features.

Going forward, new customers will serve as the foundation for further expansion. Datadog set a new high in Q2 for customer additions and finished Q2 with over 16,400 in total customers, up 36% YoY.

“Large” customers (>$100k annual revenue) currently account for 80% of total revenue. The company reported to have 1,610 “large” logos in Q2, up nearly 60% from the same quarter previous year. Two years ago, DDOG had only 594, showing that the company nearly tripled its base of large customers.

DDOG hasn’t disclosed its accurate DBNRR since IPO, but indicates that it's higher than 130% in Q2, as it had been for the previous 16 quarters. This means that clients on average raise their Datadog spending by 30% or more each year.

In Q2, for example, the number of consumers using two or more products climbed by 49% YoY, while the total number of customers increased by 36%. The absolute number of customers using four or more products jumped 2.5x YoY. As Datadog adds additional products to the platform, we'll likely see more customers adopting a larger number of them. In the first quarter of this year, Datadog revealed that “hundreds” of customers were even using six or more products.

High revenue growth is being driven by a mix of these reasons. As long as customer growth remains above 30% and the DBNRR remains over 130%, we will continue to see total revenue growth of over 50%.

Profitability

Non-GAAP gross margin in the second quarter was 76%, slightly down from 77% in Q1 and 80% a year ago. Due to ongoing platform investments, management said that gross margin is lower. This makes sense, given the company’s growing integration with hyperscalers and support for government organizations' dedicated cloud environments.

Datadog continues to show operational leverage despite increasing sales growth.

Operating income was $30.9 million, or 13% of revenue, compared to an expected range of $9 million to $11 million reflects a significant beat, owing mostly to sales outperformance. The long-term operating margin target for Datadog remains at 20% - 25%.

Most noteworthy in terms of functional areas is Datadog's ongoing ramp of R&D cost and leverage in S&M expense. In Q2, non-GAAP S&M spending climbed 33% YoY, while R&D spending increased by 85%. This is also the second quarter in a row that total R&D exceeds S&M. The company’s ability to maintain high growth while gradually reducing relative S&M investment implies a very efficient go-to-market strategy. The significant increase in R&D spending demonstrates their commitment to expanding the product platform. Datadog presently offers 12 products that are monetized. This is an increase from 9 at the start of the year.

Product

Datadog keeps adding new products to the platform stack, each of which tackles a specific use case and steadily adds value. Their product development has accelerated in recent years. While 2017 and 2018 saw one new product launch each, in 2019 and 2020 a total of seven new products were introduced.

Datadog has already released three new products in GA and two in Beta this year. A product is added to the price page once it has been released to GA. Datadog now offers 12 different products, up from nine at the end of 2020. Datadog's annual user conference, Dash, is still slated for late October. Dash took place virtually in August 2020, and it featured a number of new product updates and stand-alone services. Given the significant investment in R&D, I believe we can expect a similar pace this year. Dash could bring a few more products to GA, resulting in a 40% - 50% increase in priced products by the end of 2021.

The increased R&D spending also indicates that the company does not intend to slow down on product development. In Q2, R&D spending increased 85% YoY and surpassed S&M spending.

One area for future product opportunities is DevSecOps. While Datadog's guiding objective has been to help with the convergence of Development, Security, and Operations functions, this does not mean they have to stay in that intersection. Expanding on that core to provide tooling for each function in a broader sense opens up a lot of new product possibilities. While I believe their solutions will remain focused on the delivery of digitally enabled enterprises through modern software applications, I believe that as these organizations grow, they will require more tooling to execute along each of these separate functions.

Competitive Landscape

The market for application and infrastructure observability is huge. Datadog previously assessed it to be in the low $40 billion, but that didn't include some of their most recent product developments, especially the expanding security opportunity. Datadog's key market is IT Operations Management (ITOM), which Gartner predicts will reach $44 billion by 2024. Gartner also anticipated that just roughly 5% of applications were monitored in 2018. This ratio has increased slightly, although it is still far from critical mass.

The growth of cloud providers is a useful indicator of the rate at which cloud infrastructure is expanding, which Datadog can address. Cloud services infrastructure investment grew 36% to $47 billion in the second quarter of this year, according to market research firm Canalys, representing almost $200 billion annually. Monitoring would account for 5-10% of a typical cloud infrastructure IT expenditure, representing a $10 billion to $20 billion market opportunity. In their Q2 results, the Big 3 cloud suppliers reported even higher growth rates than 36%. AWS grew by 37%, while Azure and GCP grew by more than 50%. These factors provide substantial tailwinds for Datadog's business and explain how their rapid growth can be sustained.

Many new participants have entered this enormous market, ranging from publicly traded firms to start-ups. Several smaller providers have lately been acquired by larger publicly traded corporations, indicating that the industry is consolidating. ServiceNow and Lightstep, IBM and Instana, and Crowdstrike and Humio are a few examples. This consolidation indicates market maturity and solidifies the position of the leading players.

The observability market has become somewhat commoditized at this stage. As a result, observability companies are now being judged on the breadth of their platform offerings. Log analysis, APM, network monitoring, and synthetics are no longer viable stand-alone solutions. This explains certain recent acquisitions in which the acquiring company only addressed a few use cases. Due to the similarity of most point offerings, providers are evaluated based on the number of feature solutions they cover, with the broadest offering typically prevailing. Larger suppliers have benefited from this evolution, as their R&D budgets or balance sheets can support adding more functionalities through internal development or acquisitions.

This is likely to continue in the future. Leading suppliers will continue to enhance their solutions in order to check off more of the boxes on a CTO/observability CIO's wish list. For DevSecOps professionals, switching between several monitoring solutions is inefficient. This creates a stronger case for companies with a wholistic offering and creates significant barriers to entry for newcomers. With only a few point solutions, it's difficult to gain market share.

This also helps to understand why Datadog and some competitors have been racing to launch a slew of new services. Datadog is in a strong position due to its significant investment in R&D and well-tuned product development process. This is now essentially an execution game and the company with the best product development and go-to-market processes will win. At the moment, Datadog in command as it is outpacing all of its competitors.

DDOG is built on a solid foundation. Their founders had firsthand experience with the DevOps dilemma before founding Datadog, and they continue to lead the company today. They have an innate sense of which items will meet customer demand at the correct time. Because Datadog began in infrastructure, their Agent was able to reach every component of a customer's infrastructure. And their focus on digital disruptors provides them with a rapidly expanding customer base.

Datadog has built a finely-tuned flywheel of product development and go-to-market services around this core. They've also put a lot of emphasis on product innovation, building a product offering that can easily be expanded into adjacent markets.

At a high level, Datadog differentiates itself from competitors in the core infrastructure and application observability market through its go-to-market (GTM) leverage and product development velocity:

GTM Leverage - DDOG’s growth is driven by expansion of contracts with existing customers. New products can be easily added and require no adjustments to the infrastructure configuration. This means that Datadog does not need to scale S&M costs proportional to revenue growth. In Q2, S&M spending increased by only 33% YoY compared to revenue growth of 67%. This sales efficiency implies a significant leverage in the company’s GTM approach.

Product Development Velocity - Benefitting from its strong GTM efficiency, DDOG can invest more revenue back into R&D to drive its platform expansion.

Among its main competitors Dynatrace, Elastic, New Relic and Splunk, Datadog has the lowest S&M in % of revenue but at the same time the highest growth rate. DDOG’s R&D spend increased 85% YoY in Q2, compared to a growth range of 18% - 43% of the competition.

Also noteworthy is Datadog's ability to increase spending each year on an absolute basis due to its high annual revenue growth and increasing allocation to R&D. Except for Splunk, Datadog spent significantly more on R&D in absolute terms than all of its competitors and more than twice as much than Dynatrace.

Given their scale, Splunk is likely to be the one to keep an eye on the most. Splunk has been transitioning to a cloud service and a new pricing model, which has had an impact on revenue growth due to variations in revenue recognition. In the most recent quarter, their cloud segment generated $217 million in revenue, up 73% YoY, and accounting for 36% of total revenue.

Elastic's revenue growth has accelerated this year, jumping from 44% in the previous quarter to 50% in the most recent. Cloud revenue increased by 89% to 32% percent of total revenue (up from 25% a year ago). For the first time, they also generated a positive Non-GAAP operating margin. Customer growth and the pace of net expansion remain high. On the negative side, billings and deferred revenue growth fell this quarter, and the full-year increase was roughly the same magnitude as the Q1 increase.

Returning to Datadog, their large R&D budget is being applied in two directions. They not only introduce new products, but they also improve on old ones. As a result, Datadog has been able to “catch up” to product offers from competitors that entered the sector later. APM is a good example. Datadog was not even featured in Gartner's Magic Quadrant for APM solutions for the years 2018 and 2019 after launching their APM product in 2017. They were added to the Visionary quadrant in 2020. They were upgraded to the Leaders quadrant in 2021 and are now ranked 2nd in “Completeness of Vision” among the 5 immediate competitors, with only long-time incumbent Dynatrace ahead of them (for now).

I believe Security Information and Event Management (SIEM) will follow a similar path. Datadog released its Security Monitoring software to the general public in 2020, and since then, they've been expanding to the security platform. Gartner has a magic quadrant for the SIEM category. To be eligible, an organization must have market-proven security monitoring, threat detection, and compliance capabilities. Datadog was not listed in the Gartner magic quadrants for SIEM in 2020 and 2021. This is due to the product's maturity and the lack of a compliance solution before this year. Elastic was unexpectedly included to the magic quadrant in 2021 as a niche player. Following the APM model, I expect Datadog will be added to the SIEM MQ in the next year or two, as the product matures and its customer base expands.

As Datadog expands beyond application and infrastructure observability into security, developer workflows, and operations, certain firms in those areas are making moves that could eat into Datadog's market.

Conclusion

Datadog is putting the pedal to the metal and gaining ground this year. Their very effective flywheel of go-to-market and product development is propelling them forward. Customers are being added, spending is increasing, and new products are being released, all of which are accelerating revenue growth. This is demonstrated by the significant increase in the full-year target, with RPO and incremental ARR reaching new highs.

Datadog continues to grow its free cash flow while maintaining good margins. The efficiency of the go-to-market operation is particularly outstanding, as Sales and Marketing requires less incremental investment each year. This allows greater gross profit to be allocated to research and development. For the past two quarters, R&D has outspent S&M as a percentage of revenue. This distinguishes Datadog from its competitors, allowing it to focus more on product development.

With three new security solutions introduced recently, the pace of product releases has accelerated significantly. Datadog's new Cloud Security Platform is built on these technologies, which are combined with Security Monitoring. Datadog is expanding its product line beyond security, with additional features such as developer pipeline visibility and database monitoring. The company now has 12 independently priced items on its marketplace, with two more in beta. And, in October, we can expect Datadog to make a few new product announcements at Dash.

All of these things combine to create a strong foundation for the rest of the year.

For the full year 2021, I expect total revenue to come in at $1 billion, implying a 66% annual growth rate, given its strong customer growth and net expansion with existing logos. The median analyst estimate for 2021 revenue is $944 million, representing a 56% growth rate. This is mostly consistent with the information supplied by Datadog management in the Q2 report. Analysts predict growth of 37% and 34% in 2022 and 2023, respectively. In May, these figures were 34% and 26%, respectively, indicating that analysts have already raised their growth forecasts for the next two years in the last three months.

Datadog has a market capitalization of $42.5 billion, a share price of around $137, and an EV / LTM sales ratio of 60x. The EV / sales ratio falls to around 42 if they hit $1 billion in revenue by the end of 2021. This is still a rich multiple but the market pays a high premium for category leaders who maintain ultra-high growth at scale.

Following the Q2 results, I built a substantial stake in DDOG for my personal portfolio with a cost basis of $130. I'm comfortable keeping a high allocation in this position at least for the remaining part of 2021, given their good momentum and outlook.

Active

Pexip (PEXIP) - Target price: $15. Analysis

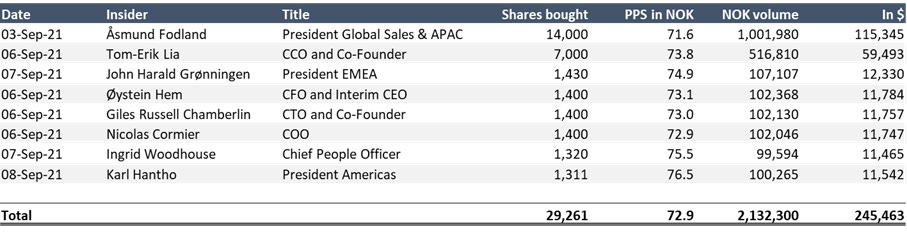

3 weeks ago, the company announced that the board had decided to pursue a change of CEO. Since then, insiders have been increasingly buying shares and the share price has climbed +23% straight up.

I continue to be bullish and maintain my price target of $15 based on good performance and a discount valuation.

ECOMI (OMI) - Analysis

NEWS | OPPORTUNITIES | BITES

🌆 The 26 most beautiful towns in the USA

🌱 One of the world’s most renowned restaurants went vegan earlier this year. Now they have a waitlist of 50,000

🏍️ If Tesla sold a motorbike

Was this forwarded to you? You can get your own copy sent to your inbox every week.

If you find this newsletter interesting and know people who might enjoy it, it would mean a lot if you forward it on 🙏

I am long PEXIP, OMI, DDOG. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

I am not a registered investment, legal or tax advisor or a broker / dealer. All investment / financial opinions expressed by me are from personal research and experience and are intended as educational material. Although best efforts are made to ensure that all information is accurate and up to date, occasionally unintended errors and misprints may occur.