Cloud News & Opportunities

NEWS | IPOS | OPPORTUNITIES | READING

Tech Regulation

2021 is already anticipated to become the year in which governments increase their efforts to regulate big tech. In another early example of this, last week Maryland launched a first-in-the-nation tax on online advertising as states across the US are trying to capture some of the profits made by tech companies throughout the pandemic. More here.

Apple vs Facebook

The animosity between Mark Zuckerberg and Tim Cook is heating up, as Mark Zuckerberg reportedly told his team "We need to inflict pain.".

Looking to control the next computer platforms, FB has introduced its Oculus headsets and the home-video-calling device Portal, and is apparently developing a competing smartwatch that it hopes to bring to market in 2021, which would increase competition with Apple.

Bitcoin

Jay-Z and Twitter founder Jack Dorsey founded an endowment called ₿trust and funded it with 500 bitcoin (around $23 million). The endowment will focus on developing bitcoin in Africa and India — India has been reluctant to welcome any kind of cryptocurrencies so far, whereas Africa (and especially Nigeria, see chart below) has seen wide adoption and a surge in transactions. The description for a job at the endowment’s board of directors states that its goal is to “make bitcoin the internet’s currency.”

A good analysis of why countries, and specifically India, would benefit from going long on cryptocurrencies.

Microsoft -> Pinterest

Over the past months, Microsoft discussed with Pinterest a potential deal to acquire the $51 billion social media platform. With its interest in TikTok, Microsoft had previously looked to online communities as a way to bring new business to its Azure cloud platform. Pinterest, which has almost 460 million MAUs, currently relies on AWS for its cloud infrastructure. Additionally, a social media platform on which users share pictures of things that interest them or which they want to buy can become an important data source for Microsoft’s marketing services and feed raw material into the company’s AI systems for training. Business Insider has more.

Clubhouse

On Saturday, Elon Musk invited Russia’s Vladimir Putin via Twitter to join him for a conversation on Clubhouse. The Tesla and SpaceX CEO then said in Russian: “It would be a great honor to speak with you.” The Kremlin told reporters on Monday that the proposal was “interesting” but more details were needed. CNBC has more.

European IPOs

Tech and ecommerce companies are the lockdown winners and attract investor money in record amounts. European IPOs had their strongest YTD since 2015 with a total of €8 billion raised. FT has more.

showing Booming start for Europe's IPO market")

As user growth soared 44% in 2020 to a daily average of 52 million, Reddit just closed a $250 million round led by Vy Capital, a Dubai-based investment firm, that values the company at $6 billion, up from $3 billion 2 years ago. Other investors participating in the round include Tencent Holdings, Andreessen Horowitz and Sequoia Capital. The CEO announced that he plans to invest the funds into areas like video, advertising, consumer products and expansion into international markets. More here.

NEWS | IPOS | OPPORTUNITIES | READING

Samsara

The San Francisco-based cloud platform for fleet management software, which raised its last round in May 2020 at a valuation of $5.4 billion, is reportedly planning to go public as soon as next month, according to Bloomberg.

Roblox

Roblox, the platform for kids’ games development is preparing for IPO and released an updated prospectus showing that Q1 - Q3 2020 revenue was higher than initially reported and its bottom line P&L more profitable. The company said it expects to go public in March. CNBC has more here.

Bumble

On Friday, bumble began trading at $43 per share, 20% above its original pricing range. Today’s closing price was $70, that’s a plus of 74% on its first day of trading.

Some background colour: Bumble was founded in 2014 by Whitney Wolfe Herd, who co-founded Tinder. She the dating app earlier in 2014 after growing tensions with several company executives and filed a lawsuit against the company based on sexual harassment. In 2018, Tinder’s parent company Match Group (MTCH), offered $450 million to acquire Bumble. Whitney Wolfe Herd, 31, is one of the youngest female CEOs to take a company public. Business Insider has more here.

Matterport

Real estate VR tech firm Matterport has announced that it is going public via a SPAC merger with blank-check company Gores Holdings VI in a transaction that values the company at $2.9 billion. Matterport is looking to raise close to $300 million from investors including Tiger Global and Fidelity. The company had previously raised $114 million from Qualcomm Ventures and others. Bloomberg has more here.

NEWS | IPOS | OPPORTUNITIES | READING

New

Pexip (PEXIP) - Target price: $30 (Long, +125% vs current PPS)

Founded in 2012 and headquartered in Oslo, Norway, Pexip offers video conferencing software and infrastructure.

Market:

When Covid-19 broke out, the business world needed a video communication solution immediately. Due to its strong brand and already $620 million in revenue at that time, Zoom was positioned well to capture a dominant share of the market.

The four market leaders are currently Zoom, Microsoft Teams, Google Meet and Cisco Webex. Their reported user numbers are at least one order of magnitude larger than any other company’s reported figure. Each company shares different types of user data, but to provide a rough comparison, MS Teams reported >115 daily active users (DAUs) at the end of October 2020, Google Meet recently reported >100 million daily meeting attendees while Zoom reported >300m daily meeting attendees (not DAUs). Finally, Cisco Webex quoted ~600 million monthly meeting attendees for October 2020. All of these figures represent 10-20x growth compared to user figures in 2019. Until 2026, the market is expected to grow at 19% annually to $50 billion with a growing adoption in education, healthcare, government and other verticals.

The four market leaders have several advantages playing in their favor, including Microsoft’s, Google’s and Cisco’s ability to package their product in wider office and enterprise productivity suites, ensuring fast adoption and sticky usage. Zoom started as a video-conferencing “pure play” but is now adding hardware solutions such as Zoom Phone. Zoom’s cloud solution was very convenient and offered the best user experience, creating the reference product for other companies. All other players have recently added functionality to match Zoom’s offering.

Security concerns grew throughout 2020 as people realized that Zoom had access to meetings’ contents. As a result, large enterprises and security conscious companies are increasingly looking for alternatives.

Product differentiation and competitive advantages:

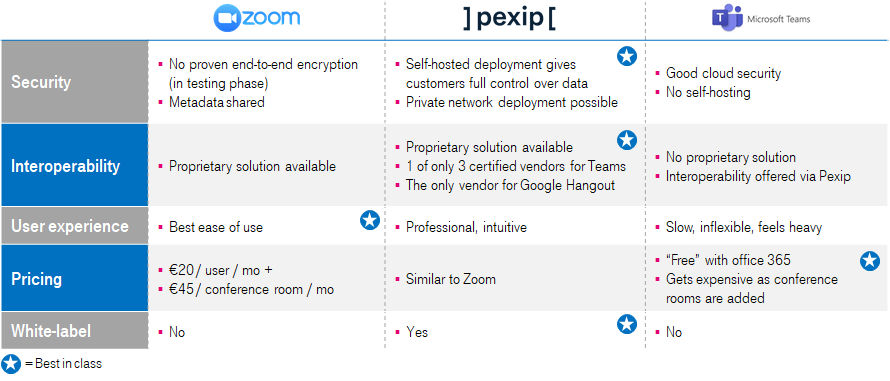

Security. Security will be an important factor with a differentiation angle for challengers, especially for customer groups dealing with sensitive data in verticals such as Healthcare, Finance, Education and Government. Zoom allegedly used fake end-to-end encryption and had access to the content of the meetings it hosted. As a result, the company saw itself banned for official business by governments and companies including Canada, Taiwan, SpaceX, NASA, school boards in New York and several others. Pexip has a focus on and competitive advantage for government and enterprise accounts due to its end-to-end security offering. Accounts include NASA, Vodafone, Spotify, Intel, Accenture, the US Defense Health Agency, the US Airforce, Deutsche Bahn and many others. Apart from being end-to-end encrypted, Pexip’s solution can be run as-a-service (hosted by Pexip), self-hosted in a public or private cloud (using own cloud provider), on-prem (self-hosted with own physical server) or even in a private network (no internet connection needed; ultimate level of privacy and security). More on privacy in this video.

Interoperability. Interoperability describes the ability to join cloud meetings of different software providers using hardware from different third-party vendors. Imagine for example, you walk into any meeting room equipped with Cisco or Poly video conferencing systems and want to join the Microsoft Teams meeting or Google Hangouts call. As lock-downs end (hopefully soon) and people return to the office, meetings will not only remain more digital, but most meetings will include videos in conference rooms. As a result, companies with a large number of conference rooms will choose a video software that is compatible with different hardware vendors. MS Teams for example does not have a proprietary interoperability solution but rather offers conference room interoperability through a Pexip gateway. This means that when conference rooms equipped with third party hardware, want to join a MS Teams meeting, they will use a Pexip gateway in the background (without knowing). As of last year, Pexip is one out of only three certified vendors to offer a Microsoft Teams cloud video interoperability solution and the only vendor to offer a Google Hangouts interoperability solution.

User experience. Ease-of-use and video quality were two factors driving Zoom’s growth. According to the October Gartner report, customers increasingly turn away from MS Teams and Cisco due to limited flexibility and user friendliness. Pexip offers an enterprise-grade video solution at scale with best in class video quality, similar to that of Zoom.

Source: Author

To summarize, for large enterprises and government organizations which have high security requirements, a large number of conference rooms and who require a high-quality video conferencing solution, Pexip has the best offering on the market and a competitive advantage.

Source: Q4-20 earnings presentation

Partnerships:

Logitech: In January, Pexip announced a partnership with Logitech, which will integrate Pexip’s Room software natively with Logitech’s video conferencing devices. According to Synergy Research, Logitech’s global (!) market share of video conferencing equipment was 17% in Q2-20.

Epic: Pexip and Epic launched a partnership for Telehealth. Epic is a major global provider of electronic patient journals for healthcare providers. With Pexip’s integration, providers can enable a video appointment as part of their existing workflows. More than 250 million patients have a current electronic patient record in Epic across a range of healthcare providers.

Financials: Pexip’s financial performance is very strong even for high-growth SaaS companies. The company published its Q4-20 results last week and continues to outperform expectations.

ARR growth: In Q4-20, Pexip reached ARR of $81.9 million, up from $47.2 million in Q4-19, representing a YoY growth of 73%. Growth was driven by a range of important customer wins both in the enterprise segment and in the public sector, including a record $2 million ARR deal with the US Defense Health Agency.

Profitability and cash: For the year 2020, Pexip’s gross margin was a first class 94%, comparing to Zoom’s 81% and the BVP Cloud Index Median of 74%. Pexip offers customers the option to host its video communication software on their own servers or in their own cloud, which reduces hosting costs for Pexip and leads to a higher gross margin. From an operational profitability perspective, Pexip had a positive EBITDA margin of 12.4% for 2020. With $132 million of net cash on the balance sheet, one could argue that the company can afford to burn more capital to increase growth. At 73%, growth is at a healthy level and sometimes accelerating too fast can do more damage than good to a company. This is not a real issue and rather the kind of problem other companies which they had.

Pexip sells through +300 channel partners, which carry much of the S&M and customer success cost. Channel partners include NTT Data, Orange, Computacenter, Telstra , Axians and many other. This structure allows Pexip to save on S&M costs which it can reinvest into product development. No channel partner represents more than 10% of revenue, implying low concentration risk in its go-to-market strategy.Rule of 40: Pexip’s rule of 40 value (a measure of balance between growth and profitability) is a very strong 71% for Q4-20. As a reference, the industry target value is 40% and the Median of Meritech’s SaaS Index is 37%.

Net expansion: In Q4, net expansion (the percent of retained revenue from existing customers) was 114% YoY, including churn of 10%. This is a good value and matched the Median of Meritech’s SaaS Index of 115%.

Valuation:

At a Total Enterprise Value (TEV) of $1.2 billion, Pexip is valued at a TEV / NTM revenue multiple of 12.0x. This compares to Zoom’s multiple of 37x. While Zoom’s higher multiple can be partially explained through higher expected growth and a premium for its market leadership position, it’s rare to see a company, which is growing 73%, which is profitable and has plenty of cash on hand, being valued at a multiple of only 12.0x; especially in today’s environment where the median for companies growing 24% is 22.6x NTM revenues.

In my opinion, one of the main reasons for Pexip’s low valuation is that the company is based in Norway and listed at the Oslo stock exchange rather than the Nasdaq. So essentially, due to a lack of awareness from the broader market. I believe that as the attention around Pexip grows, there is a large potential for multiple expansion.

In a nutshell, Pexip has a high quality video conferencing solution with a competitive advantage for a specific customer group. While I don’t believe it will replace Zoom, MS Teams, or Webex anytime soon, within its own niche, the company has the potential to become a market leader on a global scale. At a valuation of 12.0x NTM revenues, plenty of cash available and a phenomenal financial performance, the return potential relative to its risk is highly attractive. Following a fundamentals - based valuation approach, my price target for Pexip is $30, which is realistically achievable within the next 18 - 24 months.

Active

Appian (APPN) - Target price: $80 (Short, Analysis)

Short interest has decreased from over 20% to now 15%. While this is a good sign, there could be another upwards spike this week before we see a more distinct correction in the following weeks. For this reason I have taken some profits with mature investments to keep some cash as reserve and increase my short position at a potential spike this week if the opportunity arises.

Wix.com (WIX) - Target price: $350 (Long, Analysis)

I expect there will be increased selling behaviour around the $300 PPS level but at a valuation of 13.6x NTM revenue and +30% YoY growth the company is still valued well below comparable businesses. I reiterate my target price of $350 and hold on to my position, while waiting for further news around the company’s Q4 performance released this week.

NEWS | IPOS | OPPORTUNITIES | READING

Epic shows off ‘MetaHuman’ creation software.

Create your perfect girlfriend / boyfriend using AI.

Can the boom in SaaS stocks last through 2021?

Revenue from the top 100 subscription apps grew 34% to $13 billion in 2020.

Spotted my dream apartment. And I only need $46m (more) to buy it.

Was this forwarded to you? Sign up, and get your own copy of Cloud News & Opportunities sent to your inbox every week.

Feedback, comments or questions are always appreciated and if you know people who might enjoy the newsletter, it would mean a lot if you forward it on.

Disclosure: I am long PEXIP and WIX, and short APPN. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it other than from paid subscribers of my newsletter. I have no business relationship with any company whose stock is mentioned in this article.

Disclaimer: I am not a registered investment, legal or tax advisor or a broker / dealer. All investment / financial opinions expressed by me are from personal research and experience and are intended as educational material. Although best efforts are made to ensure that all information is accurate and up to date, occasionally unintended errors and misprints may occur.